Call and Put Options in the Stock Market: Structure, Purpose, and Strategic Use for Traders Explained

Call and put options in the stock market represent one of the most flexible and strategically powerful financial tools available to traders, enabling them to speculate, hedge risk, generate income, or leverage capital with greater precision than ordinary share transactions. While a stock purchase conveys direct ownership of shares, an option conveys the right—but never the obligation—to buy or sell shares at a predetermined price in the future. This key distinction provides traders with opportunities to capitalize on price movement without committing to full stock ownership, and to protect portfolios against sharp market fluctuations. Understanding call and put options requires exploring how they work, what rights they grant, how traders interpret their market signals, and how option pricing reflects expectations about volatility and directional bias. When interpreted properly, call and put options become not merely speculative tools but structured contracts that mirror the psychological and economic forces that govern broader market behavior.

A call option is a financial contract that gives the buyer the right to purchase an underlying asset—such as a stock—at a predetermined price known as the strike price before a set expiration date. Call buyers seek to profit from expected upward price moves because as the price of the stock rises above the strike price, the call option increases in value. For example, if a trader purchases a call option with a strike price of $100 and the stock rises to $130 before expiration, the call has intrinsic value because the trader now has the right to buy at $100—well below market value. The buyer may either exercise the option to acquire the stock at the strike price or sell the option contract itself at a higher price to another market participant. Conversely, if the stock never rises above the strike price, the option expires worthless and the trader loses only the premium paid. This asymmetric payoff—limited downside risk but potentially large upside gain—is what attracts many traders to calls. Meanwhile, the seller of a call—known as the writer—receives the premium and profits if the option expires without being exercised, but may face substantial risk if the stock rallies sharply. For this reason, writing uncovered (or “naked”) calls is considered a high-risk strategy, whereas writing covered calls—selling calls against shares already owned—is used by many investors as a conservative method of generating regular income.

A put option, in contrast, gives the buyer the right to sell the underlying stock at the strike price before expiration. Put buyers generally expect the price of the stock to fall because the put gains value as the stock declines. If a trader buys a put option with a strike price of $100 and the stock falls to $70, the option becomes profitable because it grants the right to sell at $100 despite the market price being $30 lower. The buyer can exercise the option or sell it to another trader at an increased premium. If the stock remains above the strike price through expiration, the put loses value and may expire worthless, limiting the buyer’s loss to the initial premium. From a risk management standpoint, puts are powerful hedging tools because they act as portfolio insurance; a long-term investor who owns shares can buy puts to protect their holdings during periods of uncertainty. The seller of a put takes on the obligation to purchase the stock at the strike price if the option is exercised. Put writing is often used by value-oriented investors who want to acquire shares at a lower effective price—the premium they receive reduces the net cost if they end up buying the stock, while allowing income generation if the option expires unused.

The pricing of calls and puts is rooted in expectations about volatility, time to expiration, and directional bias, which reflect the interplay of market sentiment and mathematical probability. An option’s premium consists of intrinsic value, the portion based on the relationship between strike price and market price, and time value, which represents the potential for the option to become profitable before expiration. Time value decays with each passing day—an effect known as theta decay—which benefits option sellers and challenges option buyers. Volatility, both historical and implied, strongly influences option prices, as large price swings increase the probability of the option ending “in the money.” Because implied volatility reflects anticipated uncertainty rather than current price movement, dramatic increases in option premiums can occur even when the underlying stock has barely moved, demonstrating that options encode expectations as much as they encode current price. Traders who grasp the dynamics of volatility, time decay, and directional risk understand that the most successful option strategies depend not only on forecasting price direction but also on evaluating how long it may take for that forecast to unfold and how aggressively the market expects price to move.

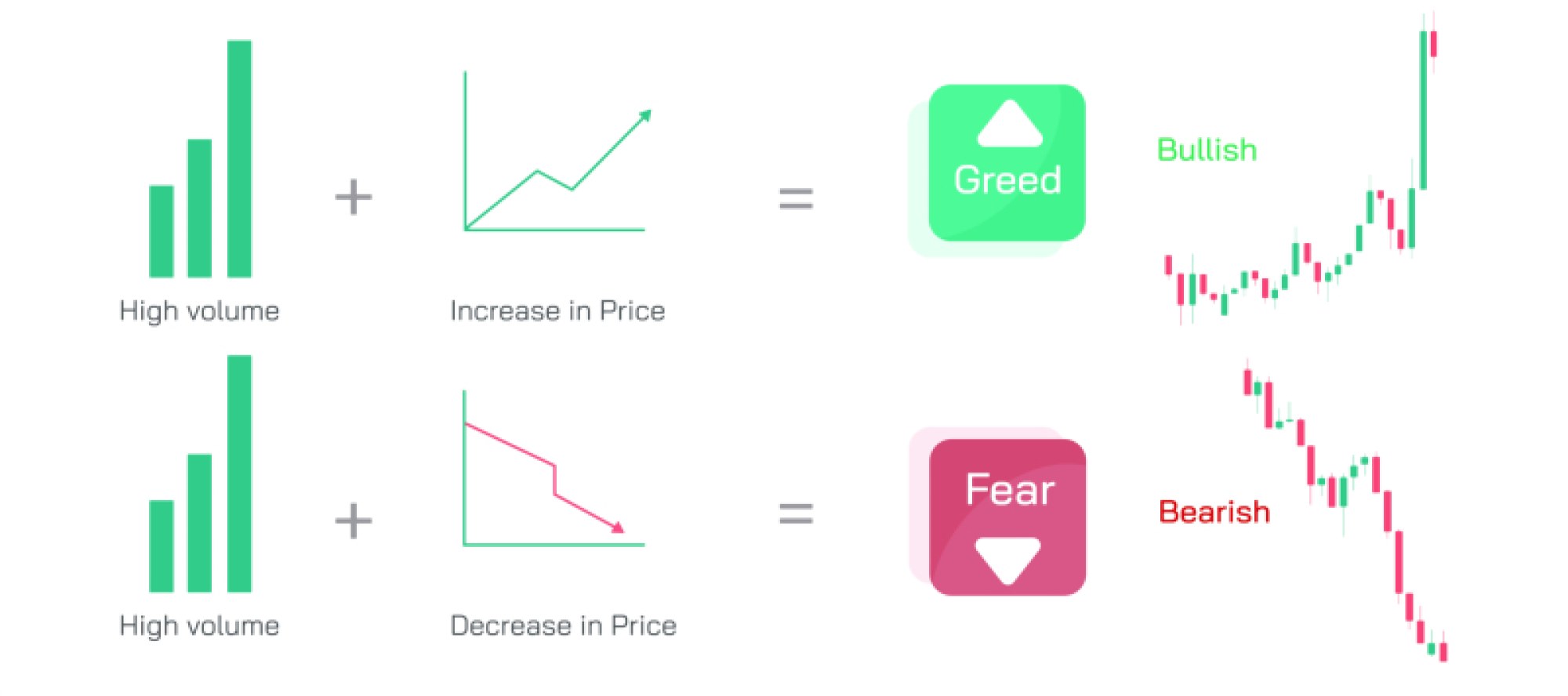

The strategic use of calls and puts extends far beyond simple bullish or bearish speculation. Options enable traders to construct multi-legged strategies that express nuanced market views. For example, traders may sell covered calls to generate income, buy protective puts to hedge long stock positions, execute vertical spreads to limit risk while targeting directional moves, or combine calls and puts to capitalize on volatility rather than direction. The presence of calls and puts in the market also provides information about trader sentiment and liquidity positioning. A surge in call buying may signal widespread bullish speculation or institutional hedging against short positions, whereas heightened put activity may signal fear or preparation for downside volatility. However, interpreting these signals requires caution because institutional traders often use calls and puts in the opposite way retail traders assume; for example, selling put options may reflect bullish accumulation rather than bearish speculation because the put writer intends to acquire stock. Similarly, heavy call selling may occur not because traders expect decline but because holders of large positions are generating income while maintaining bullish exposure. Options therefore unveil the complexity of market behavior, where motivations may differ dramatically even when traders engage with the same contract type.

The position of calls and puts relative to market structure plays a distinctive role in price dynamics. Expiration dates can generate temporary volatility because large clusters of open contracts create liquidity magnets at key strike prices. If many calls or puts are “in the money,” market makers may hedge exposure by buying or selling the underlying shares, influencing near-term direction. Similarly, the presence of massive open interest at a strike price can function as temporary support or resistance because price gravitates toward levels that minimize payout obligations—a behavior often described as “pinning”. During major expiration events—such as monthly or quarterly expiries—these forces amplify, helping to explain sudden price flattening or reversal near prominent strike prices.

At the psychological level, call and put options demonstrate how risk perception and expectations drive trader behavior. The appeal of calls stems from the possibility of outsized gains with limited loss, mirroring optimism and growth-oriented speculation. Puts reflect caution, skepticism, and security seeking, embodying the protective instinct that arises when uncertainty increases. Yet the most skilled market participants learn to balance these tools not to amplify emotion but to neutralize it—using calls and puts to manage probability rather than to express hope or fear. Options, when applied thoughtfully, transform the market from a one-dimensional contest of price prediction into a strategic landscape where timing, volatility expectations, and risk tolerance shape every decision.

Ultimately, call and put options serve as a sophisticated extension of the stock market’s core function—the matching of buyers and sellers based on perceived value. A call reflects the desire to purchase future value; a put reflects the right to transfer risk. Together, they enable liquidity to flow more efficiently, provide mechanisms for speculation and protection, and create a deeper marketplace where pricing is not merely a snapshot of current belief but an ongoing negotiation about the future. For traders who take time to understand the structure, logic, and psychology behind options, call and put contracts become more than visual icons on a chart—they become lenses through which the mechanics of the market, and the motivations of its participants, can be understood at a more profound level.