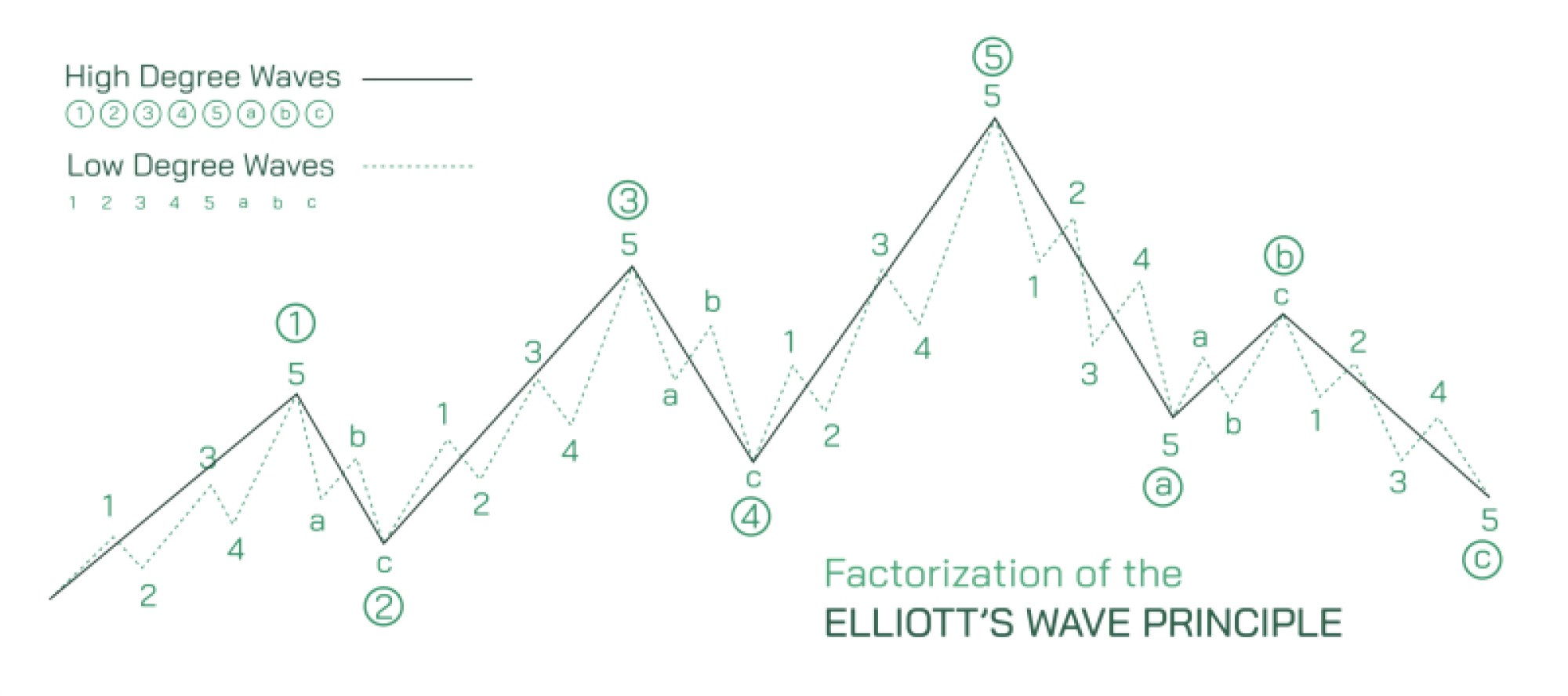

Stock Market Options Trading Strategies: Profit Maximization and Risk Management Explained

Options trading stands out in the stock market because it allows traders to design outcomes that cannot be achieved through direct share ownership alone. With options, market participants can generate income, hedge against risk, profit from directional speculation, benefit from sideways price movement, or even exploit volatility without caring about whether price goes up or down. This flexibility is what makes options more than speculative tools—they are strategic contracts that enable traders to mold risk and reward according to their forecast, capital, and risk tolerance. But the same flexibility that makes options powerful can also make them dangerous when misunderstood, because leverage magnifies both profits and losses. To use options effectively, traders must understand the structure of different strategies and how they work to maximize profit while minimizing risk. The objective is not simply to guess market direction but to construct positions that align probability, time decay, price movement, volatility shifts, and risk controls into one coherent plan.

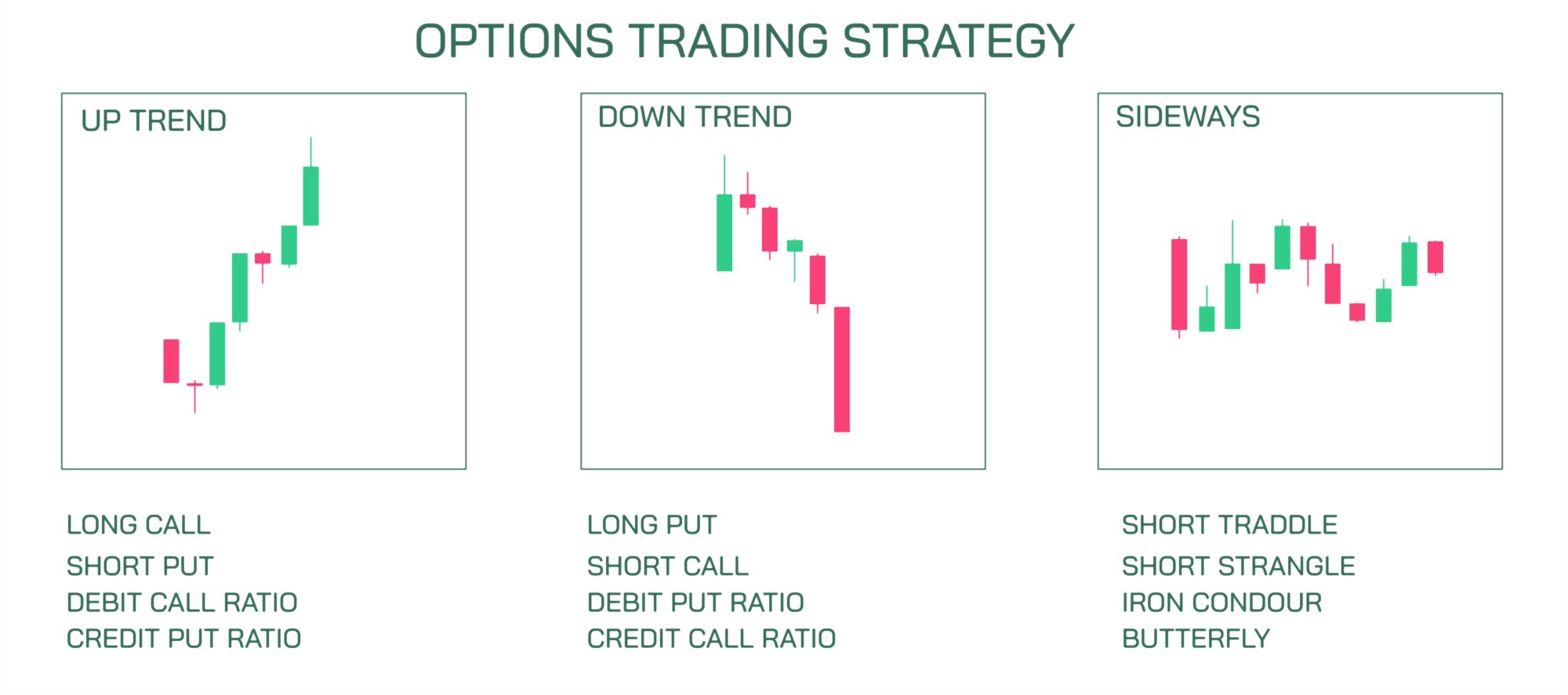

Options strategies fall into two broad categories: debit strategies, in which the trader pays a premium to open a position, and credit strategies, in which the trader receives a premium upfront and assumes an obligation. Debit strategies traditionally offer defined risk and potentially large reward, while credit strategies provide limited profit but high probability of success through income generation. The trader’s choice depends on whether they want to risk small for a chance at large returns or accept smaller gains in exchange for disciplined probability and controlled exposure. Long calls and long puts belong to debit strategies because they require buying an option. Covered calls, cash-secured puts, and credit spreads belong to credit strategies because they involve selling options. Beyond these basic forms, more complex multi-leg strategies combine calls and puts to shape payoff curves that respond precisely to specific market conditions.

One of the most well-known and widely used strategies is the covered call, a conservative income-generating technique where a trader who already owns shares sells call options against the stock. The premium collected from the call cushions mild price declines, and if the stock remains below the strike price, the trader keeps both shares and premium. If the stock rises above the strike price, the trader sells the shares at the strike price and gives up further upside—an acceptable trade-off for many investors seeking consistent cashflow. The equivalent strategy on the downside is the cash-secured put, where a trader sells a put option while holding enough cash to buy the shares if assigned. In this case, the trader collects premium and potentially acquires shares at a discount if the stock declines to the strike price. Both strategies shift options from pure speculation into risk-managed yield generation, proving that options are as useful to conservative investors as they are to aggressive traders.

Where traders seek directional exposure with lower upfront capital, long calls and long puts dominate. A long call profits when the stock price rises above the strike price by more than the premium paid, while a long put profits when the stock drops below the strike price by more than the premium cost. These positions provide asymmetric payoffs—with limited risk (the premium) but potentially sizable reward—yet they are sensitive to the passage of time because every day that the stock fails to move decisively results in premium decay. Many beginners lose money on options not because their direction was wrong but because they underestimated the time required for their idea to play out. This is why directional traders often adopt vertical spreads, which reduce the premium cost by selling another option against the long position. For example, a bull call spread combines buying a call at one strike and selling a higher-strike call—a structure that profits from upward movement while limiting risk and reducing the premium paid. Similarly, a bear put spread profits from downward movement while limiting cost by selling a lower-strike put against the long put. These spreads reduce maximum reward but greatly increase efficiency because the break-even point becomes more attainable and time decay works less aggressively against the trader.

The next category of strategies focuses not on price direction but on volatility behavior, recognizing that options pricing is heavily influenced by expected volatility. Traders who anticipate sharp movement—regardless of whether price rises or falls—often turn to straddles and strangles, which involve buying both a call and a put. A long straddle uses the same strike for both options, while a long strangle uses out-of-the-money options for lower cost. These strategies profit when the stock moves far enough in either direction to overcome the combined premium paid, making them ideal for earnings announcements, economic reports, or major news events. Conversely, when volatility is expected to contract rather than expand, traders employ iron condors and iron butterflies, which combine selling both a call spread and a put spread to collect premium from a market expected to remain within a defined range. These credit-based volatility strategies create income while establishing maximum risk boundaries on both sides of price. Because the goal is for time decay to erode total option value, these structures reward patience and risk control rather than speculation.

Another dimension of options trading involves hedging and risk reduction, which plays a fundamental role in professional portfolio management. For long-term investors, the most common hedge is the protective put, where a trader buys a put option to insure shares against a sudden drop. This allows investors to remain invested without selling immediately due to fear of temporary volatility. For traders who hold short positions, protective calls serve as a hedge against a sudden rally. These techniques show that options can transform portfolios from static exposures into controlled and adaptable instruments. Combining hedging with income generation leads to collars, where a trader holding stock buys a protective put while simultaneously selling a covered call to offset the put’s cost. Collars limit both upside and downside in exchange for stability and predictability, making them attractive during turbulent markets.

Regardless of strategy, the most important principle in options trading is risk management, because leverage magnifies both gains and losses. Every strategy must define maximum risk, maximum profit, and break-even levels before execution, not after. Traders who buy options without planning exit criteria often fall victim to time decay and unrealistic expectations. Traders who sell options without understanding assignment risk can face losses far exceeding the premium collected. This is why sophisticated traders choose strategies that fit market structure and volatility conditions instead of chasing forecasts of price direction. When volatility is low but expected to rise, debit strategies such as long calls, long puts, straddles, and strangles are appropriate. When volatility is high and expected to fall, credit strategies such as covered calls, cash-secured puts, iron condors, and iron butterflies are advantageous. When trends are strong, vertical spreads help balance risk and reward. When uncertainty is high, hedging protects capital and stabilizes emotions.

Options trading cannot be mastered through chart patterns alone because its core components—time decay, volatility, directional bias, and liquidity—interact dynamically. A trader may correctly forecast price movement but lose due to decaying option premium or collapsing volatility. Another trader may be wrong about price direction but still profit because they designed a structure that rewarded sideways movement. The most successful options traders think in terms of probability rather than prediction. Instead of asking, “Will the stock go up or down?”, they ask, “What is the most likely behavior the market will display, and what option strategy best matches that condition?”. This shift from forecasting to engineering transforms options from gambling into disciplined decision-making.

Ultimately, options trading is not about chasing the highest possible return but about shaping risk and reward deliberately. Every strategy—whether simple or complex—represents a philosophy of market participation. Some reward conviction, some reward patience, some reward volatility, and others reward balance. What unifies them all is that options give traders the freedom to participate in markets on their own terms rather than the market’s terms. With structured planning, emotional discipline, and proper risk control, options evolve from complicated instruments into precision tools—allowing traders to maximize profit when opportunities appear and minimize damage when uncertainty dominates.